Africa’s digital infrastructure footprint is expanding rapidly, yet its position in the global compute landscape is weakening. Over the past two years, the continent’s share of global compute capacity has fallen by roughly 20%, even as new subsea cables have landed, terrestrial fiber networks have expanded and additional data center capacity has come online across several major markets. The shift reflects not a slowdown in African investment, but the far faster acceleration of hyperscale and AI-driven infrastructure deployment elsewhere in the world.

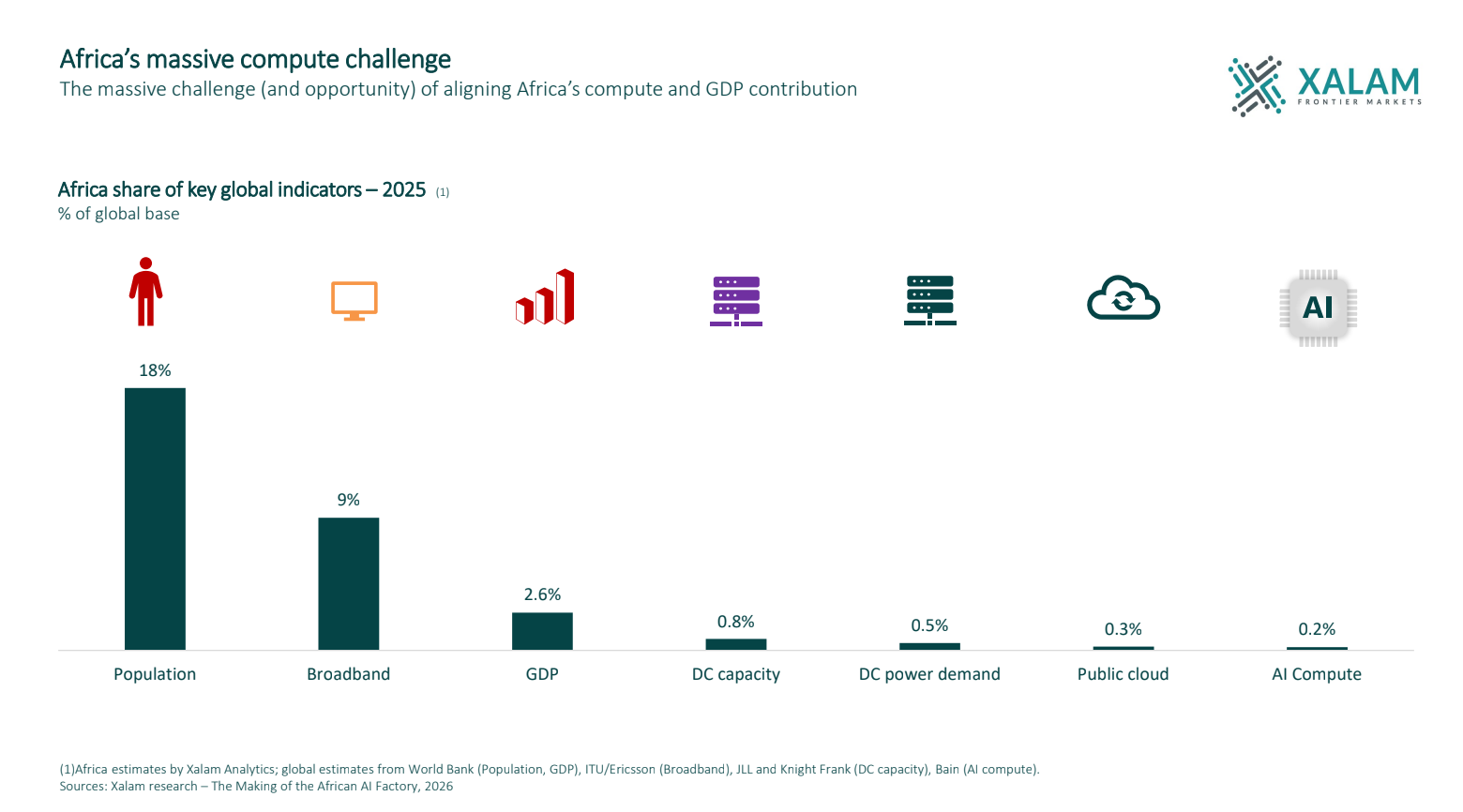

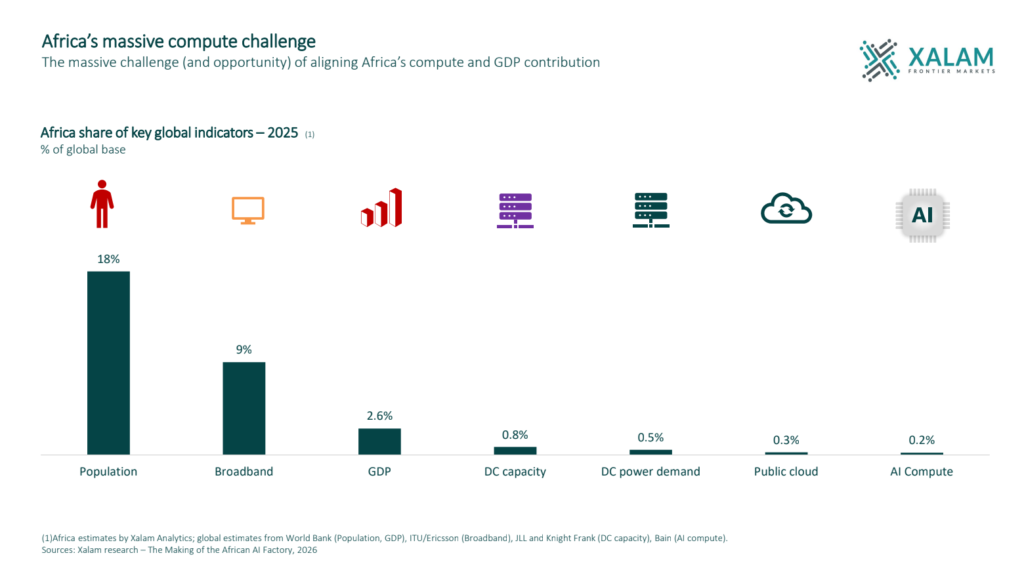

Africa today hosts roughly 500 to 600 megawatts of live data center IT capacity, part of a broader ecosystem that includes about 60 subsea cables, 145 landing points, approximately 1.4 million kilometers of terrestrial fiber and around 150 cloud and CDN points of presence. The region’s digital infrastructure is deeper and more resilient than at any point in its history. Still, Africa represents less than 1% of global data center capacity despite accounting for about 18% of the world’s population.

Global investment in compute infrastructure has entered a new phase driven by artificial intelligence workloads, hyperscale cloud expansion and power-anchored data center campuses. In the United States, Europe, the Gulf and parts of Asia, operators are deploying capacity at gigawatt scale. These deployments are reshaping the distribution of global compute faster than emerging markets can keep pace.

As compute becomes the primary infrastructure layer for artificial intelligence, financial services and digital trade, relative capacity share increasingly determines where economic value is created rather than merely where data is stored.

As Guy Zibi, Managing Partner at Xalam Analytics, observed during a recent Africa Hyperscalers conversation, the key distinction is between absolute growth and relative share. Africa’s infrastructure base is expanding, but global compute capacity is expanding faster.

This shift is already visible across multiple layers of the compute stack.

The continent accounts for roughly 0.8% of global data center capacity, down from about 1% in 2024, alongside roughly 0.3% of public cloud usage and approximately 0.2% of global AI compute resources. These figures are not declining because infrastructure investment has slowed. They are declining because investment elsewhere has accelerated dramatically.

In this context, the question facing African policymakers and investors is not whether infrastructure is being built. It is whether enough local demand is being formed to justify sustained expansion at scale.

Meaningful connectivity has improved sharply over the past decade. Roughly 700 million Africans now use 4G, 5G or fiber-based broadband, a figure expected to exceed one billion before the end of the decade. But connectivity alone does not create compute markets. Persistent workloads do.

Across most regions globally, large-scale compute infrastructure follows the concentration of enterprise applications, government platforms, financial services systems and digital consumer ecosystems. Where those workloads localize, infrastructure deepens. Where they remain distributed offshore, local capacity grows more slowly.

This helps explain why hyperscaler cloud regions remain limited across much of the continent despite clear progress in connectivity and data center investment. Cloud availability has expanded through edge nodes and partner facilities in several markets, but full regions typically emerge only after sustained workload density reaches a threshold that supports long-term deployment.

The expansion of artificial intelligence infrastructure globally is reinforcing this dynamic. AI workloads are significantly more compute-intensive than traditional enterprise applications and are driving a wave of investment concentrated in markets with abundant power availability, deep capital pools and established cloud ecosystems. As these deployments accelerate, they are increasing the denominator against which Africa’s compute footprint is measured.

The implication is not that Africa must compete at hyperscale to remain relevant. It is that the continent must prioritize converting connectivity growth into local workload concentration.

Public-sector digitization will play an important role in this transition. National identity platforms, payment infrastructure, regulatory systems and health information architectures represent some of the largest sources of structured data on the continent. When these systems are hosted locally, they provide stable baseline demand that supports infrastructure investment. Private-sector platforms are beginning to reinforce this trend. Fintech companies, digital commerce platforms and mobile financial services providers process millions of transactions daily across African markets, generating continuous streams of data that increasingly require local storage, processing and analytics.

Infrastructure investment follows usage.

Africa’s digital infrastructure pipeline remains strong, and capacity will continue to expand across major hubs including Johannesburg, Lagos, Nairobi, Cairo and Casablanca. But the next phase of growth will depend less on announcements of new facilities than on the localization of workloads that justify them.

The continent’s position in the global compute landscape is not determined only by how much infrastructure is built. It is determined by how much infrastructure is used locally.

Africa’s share of global compute will not be determined by how many cables land on its shores, how extensive its connectivity networks become, or how many facilities are announced in its cities. It will be determined by where African governments, enterprises, and digital platforms choose to run their workloads.