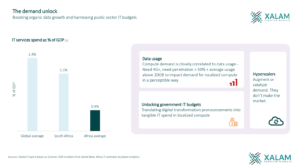

For more than a century, Kenya has been East Africa’s physical gateway. Cargo entering the Port of Mombasa has supplied markets across Uganda, Rwanda, South Sudan and eastern Democratic Republic of Congo, making the country the region’s primary logistics corridor to the global economy. Even today, during periods of geopolitical tension affecting Gulf shipping routes – including disruptions linked to Iran–US confrontation – high-value imports such as luxury vehicles bound for Middle Eastern markets have reportedly been staged through Kenyan logistics channels, underscoring the country’s role as a trusted transit platform between continents.

The question now is whether Kenya can convert that geographic inheritance into digital leverage.

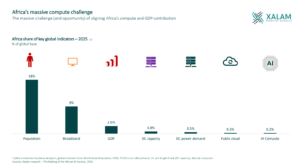

Across Africa, connectivity infrastructure is expanding rapidly. Subsea cables are landing, fiber corridors are extending inland, and new data centers are opening across major capitals. Yet the continent’s share of global compute capacity has fallen from roughly 1% to about 0.8% in just two years. The constraint has moved from bandwidth to the localization of workloads that justify large-scale infrastructure investment. As Guy Zibi, Managing Partner at Xalam Analytics, observed during a recent Africa Hyperscalers discussion, the distinction shaping Africa’s digital future is not between markets with connectivity and those without it, but between those that convert connectivity into compute and those that remain transit corridors for someone else’s infrastructure economy.

Kenya is attempting to position itself on the right side of that divide.

The country already sits at one of Africa’s most strategically important digital crossroads. Multiple international submarine cable systems land along its coast. Terrestrial fiber routes extend north toward Ethiopia, west toward Uganda and Rwanda, and south toward Tanzania. Nairobi has emerged as a regional interconnection marketplace where operators, content platforms and enterprises exchange traffic that once left the continent before returning.

According to Emmanuel Makina, Country Sales Manager for Kenya and Rwanda at PAIX Data Centres, the significance of Nairobi lies not simply in connectivity volume but in aggregation. Carrier-neutral interconnection environments allow regional traffic to remain local, reduce latency across East Africa and make the city a logical exchange point between inland markets and global networks. In emerging compute ecosystems, that interconnection density is often the first signal that a market is transitioning from connectivity access to infrastructure gravity.

Makina noted that as regional networks expand deeper into inland markets such as Uganda, Rwanda and eastern DRC, the need for neutral interconnection facilities in Nairobi is increasing. These facilities allow operators to peer directly with each other, connect to global content platforms and distribute traffic more efficiently across borders. Over time, this kind of ecosystem transforms a connected city into a regional digital hub.

Government policy is now reinforcing that transition.

Kenya’s National Digital Master Plan (2022–2032) places digital infrastructure alongside digital government, digital business and digital skills as pillars of national economic transformation. The Kenya Cloud Policy (2024) establishes a cloud-first posture across public institutions while promoting data sovereignty, residency and localization. Together, these policies signal that the state intends to anchor demand domestically rather than rely exclusively on offshore infrastructure environments.

That matters more than new cable landings.

Across emerging compute markets globally, public-sector platforms often provide the earliest stable foundation for infrastructure ecosystems. Identity systems, tax platforms, payment rails, health architectures and regulatory databases generate persistent demand that investors can model over long horizons. Where governments localize those workloads, infrastructure deepens. Where they do not, connectivity remains transit infrastructure rather than value-capture infrastructure.

Kenya’s emerging data-center strategy reflects this logic. The government is moving to designate data centers as Special Economic Zone infrastructure, a shift that would improve tax treatment, accelerate permitting and strengthen access to power for operators building large-scale facilities. In practice, SEZ designation signals that compute capacity is being treated as export-grade national infrastructure rather than purely commercial real estate.

Cabinet Secretary for Information, Communications and the Digital Economy William Kabogo has framed the transition in those terms. The government’s Bottom-Up Economic Transformation Agenda, he said, depends on digital infrastructure that can support e-commerce, e-health, e-learning and digital trade at scale.

“Data centers are the enablers of the invisible infrastructure that makes digital economies possible,” Kabogo noted, adding that Kenya intends to serve as a gateway to Africa’s digital economy through partnerships between government and private operators aligned with continental priorities such as AU Agenda 2063.

The Kenya Cloud Policy is intended to support that ambition by ensuring public workloads remain locally anchored. Meanwhile, the country’s National Artificial Intelligence Strategy explicitly links future productivity gains to the availability of domestic compute environments capable of supporting high-performance workloads across healthcare, agriculture, education, manufacturing and public administration. Facilities such as the Nxtra Airtel Africa Data Centre are expected to form part of that backbone.

Taken together, these initiatives suggest a coordinated attempt to do what only a small number of African markets have begun to achieve: convert connectivity advantage into compute permanence.

The distinction matters.

Across much of Africa, subsea capacity is expanding faster than domestic data-center ecosystems can absorb it. Countries that remain landing points risk exporting traffic rather than hosting it. Those that localize workloads capture the economic value generated by cloud adoption, digital finance, artificial intelligence and platform services.

For decades, Kenya’s ports determined how goods entered East Africa. Increasingly, its interconnection exchanges, carrier-neutral facilities and cloud infrastructure policies may determine how data does. The countries that convert connectivity into compute will shape Africa’s digital trade geography in the decades ahead. Kenya is positioning itself to be one of them.