Africa is laying the digital equivalent of highways at record speed—and importing almost everything that matters once the traffic arrives.

The continent’s connectivity story has turned a corner. Subsea systems have multiplied. Across subsea connectivity, more than 50 new cable landing points have come online, bringing in excess of 200 terabits of design international capacity to African shores. Terrestrial fiber has pushed deeper inland, as more than 300,000 kilometers of fiber have been deployed over the past five years, moving fiber-to-the-home from a luxury to a competitive battleground. This has materially strengthened network resilience and enabled the expansion of 4G and fiber-to-the-home in a growing number of markets.

Across 4G, 5G, and FTTH networks, meaningful connectivity in Africa has nearly tripled since 2020. Estimates indicate approximately 700 million meaningful connections across the continent today, with that figure expected to exceed one billion by 2030.

At the Africa Digital Infrastructure Outlook session hosted by Africa Hyperscalers, Guy Zibi,Managing Partner, Xalam Analytics stressed in his keynote: Africa’s digital infrastructure is “deeper and more resilient than it has ever been.”

But the infrastructure layer that captures the most value from connectivity – local compute – is not scaling at the same pace.

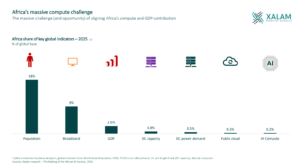

Africa is home to roughly a sixth of humanity. Yet by several credible public measures, the continent remains a rounding error in global compute. A recent Financial Times letter on the AI divide cited Africa as having less than 1% of global data center capacity – a stark indicator of how little of the world’s digital production stack sits on African soil.

This has moved from a echnology gap to a balance-of-power problem: a future in which African demand surges, but the continent continues to export the highest-margin layer of the digital economy – processing, inference, storage, and the platforms built on top of them – to other jurisdictions.

The new dependency is being manufactured by success

The keynote framed the dynamic with a blunt metric: “meaningful connectivity” – always-available, affordable access delivering at least 20 Mbps. Since 2020, meaningful connectivity has nearly tripled, with an estimated 700 million such connections today and a projected path beyond one billion by 2030, according to the presentation.

That matters because connectivity drives traffic. And traffic changes everything: it pulls content closer to users; it makes edge caching and cloud regions rational; it shortens the payback period on neutral-host facilities; it raises the opportunity cost of offshore hosting; and it expands the set of services that become viable – from real-time payments to telemedicine to AI copilots.

Here’s the paradox: Africa is growing the demand substrate for compute faster than it is building the compute itself. The continent risks recreating the commodity trap – exporting raw demand and importing finished digital value.

Why compute lags: four constraints, one political economy

The keynote distilled the market into four paradoxes – supply, demand, hyperscalers, and power. Each points to a single underlying truth: compute does not fail in Africa because of a lack of aspiration. It fails because of bankability.

Start with power, the least glamorous but most decisive variable. Data centers do not require “electricity” in the abstract. They require reliable delivery, predictable pricing, and bankable contracting structures. Across advanced markets, power scarcity is now a binding constraint on new data center supply, even when demand is strong – a warning of how quickly grid and permitting constraints can throttle the compute economy.

Africa’s grids face an even more basic challenge: reliability. The keynote captured it in a line that should become a thesis for policymakers: power may exist as national capacity, but not as dependable delivery at the meter. The result is a cost stack filled with self-provisioned generation, redundant systems, fuel logistics, and FX exposure – all of which inflate prices and lengthen payback.

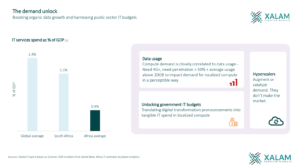

Now add capital. The keynote estimate – roughly $2bn per year in data center capex by 2030, rising to $3–4bn when IT compute is included – is not implausible when compared with what African telecom operators already spend annually. The question is not whether the continent can mobilize that quantum of capital; it’s whether investors can underwrite the risk.

And those risks are real: currency convertibility, offtake uncertainty, delayed enterprise migrations, inconsistent right-of-way regimes for fiber, and opaque permitting. These are not “Africa problems.” They are contract problems – and contract problems are solvable when governments decide compute is strategic.

The hyperscaler mirage – and the right way to think about it

Africa’s tech discourse often treats hyperscalers as saviors: “If they build regions, the ecosystem will follow.” The keynote offered the inversion: hyperscalers follow demand rather than create it. Hyperscalers invest where they can see durable demand, predictable power, and interconnection depth – and where the regulatory posture does not create open-ended compliance risk.

And this has become a sovereignty question: the world is entering an era where AI capacity and data infrastructure shape economic autonomy. Africa’s risk is not simply being “behind.” It is being locked into an upstream role in the AI economy – consumption without production.

The policy move that changes everything: demand formation

If Africa wants to capture compute value, it must manufacture demand certainty.

The fastest lever is the one most governments underuse: public sector demand. Governments can act as anchor tenants for cloud and sovereign compute, through procurement reform, shared-service architectures, and a disciplined migration plan for high-value workloads.

If done credibly, that becomes a market signal. It reduces offtake risk. It supports project finance. It justifies metro fiber diversity. It brings content and CDN nodes closer. It turns connectivity growth into compute investment – and compute investment into jobs, tax revenue, and platform innovation.

Africa is not short of cables. It is short of credible, repeatable execution frameworks that convert connectivity into local compute – and local compute into national capability.

The continent’s digital highways are filling up. The question is who is collecting the fees.