In the heart of Lagos, a Nigerian fintech company clears millions of transactions each day. The customers are African. The merchants are African. The capital circulates within African banks.

But its data – the most valuable byproduct of that activity – often travels thousands of miles before it is stored, analyzed, and monetized.

It leaves the continent.

That quiet migration captures the defining contradiction of Africa’s digital moment: a continent generating extraordinary digital demand, yet lacking the infrastructure density to contain and capitalize on it.

Over the past decade, and particularly in the last five years, Africa has laid down the arteries of a connected society. More than 50 new subsea landing points now ring its coastline, injecting over 200 terabits of international capacity into markets once constrained by bandwidth scarcity. An estimated 300,000 kilometers of terrestrial fiber have been deployed, stitching together cities and corridors that once operated in isolation. Data centers have doubled in capacity and matured from modest carrier hotels into interconnected Tier III+ facilities capable of hosting cloud and enterprise workloads.

Connectivity, long the bottleneck, is no longer the limiting factor.

Demand is accelerating.

Capacity is not.

Connectivity Is No Longer the Binding Constraint

For much of the past decade, Africa’s digital constraints were obvious: limited coverage, slow speeds, high costs. That era is receding.

4G coverage has expanded rapidly across urban and peri-urban markets. Early 5G networks are emerging. Fiber backbones now extend deeper into national economies. International bandwidth, once rationed, is abundant by historical standards.

More important than coverage is quality. “Meaningful connectivity” (a term coined by Xalam Analytics) refers to affordable, always-on broadband at speeds sufficient for real digital participation – has nearly tripled since 2020, reaching roughly 700 million Africans. Within this decade, that number could exceed one billion.

And traffic follows quality.

When connectivity becomes reliable, digital behavior intensifies. Streaming replaces broadcast. Fintech replaces cash. Cloud-based enterprise systems replace on-premise servers. AI-enabled tools begin to enter daily workflows. Governments digitize identity systems and public services.

Across finance, telecoms, media, retail, and public administration, digitization is no longer theoretical.

From a demand perspective, the signal is unmistakable.

Africa is not digitally dormant. It is digitally awakening at scale.

Rising Demand… Lagging Capacity

Yet beneath this momentum lies a stark imbalance.

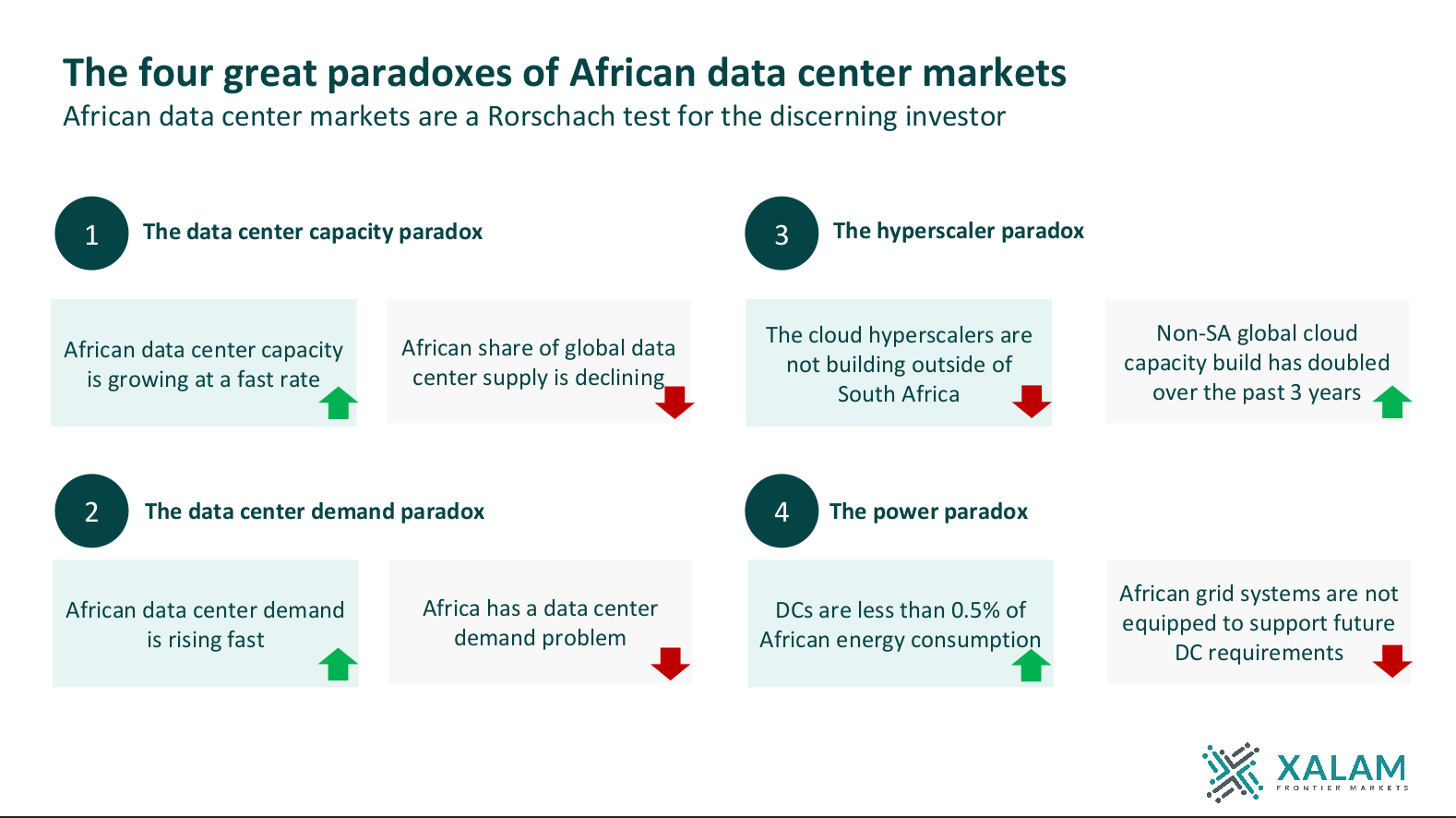

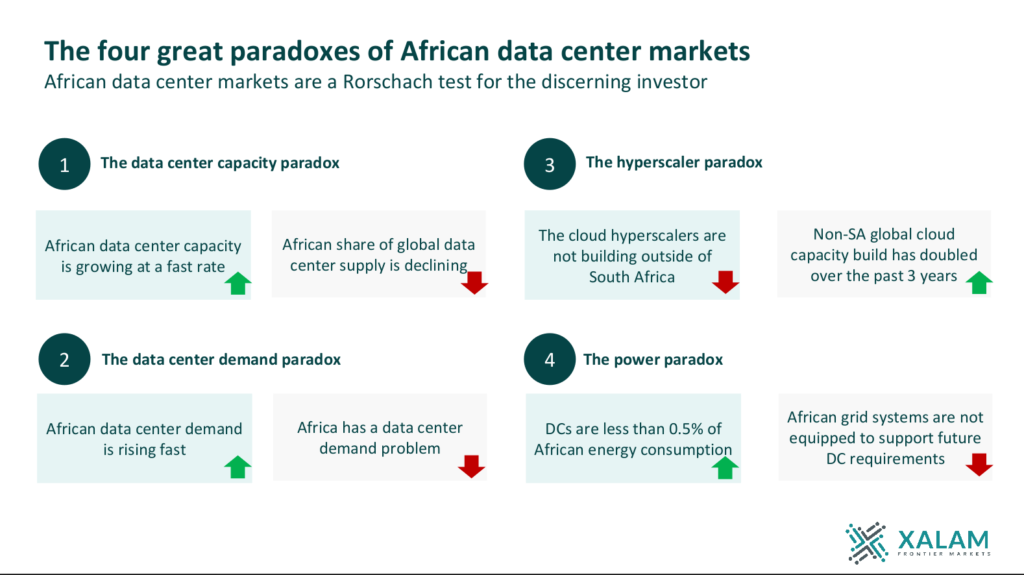

Across a continent of nearly 1.4 billion people, live data center capacity is estimated at roughly 300 to 500 megawatts of IT load. Even at the upper bound, Africa accounts for well under 1 percent of global data center capacity. North America and parts of Asia measure capacity in tens of gigawatts. Africa measures it in hundreds of megawatts.

Most of that limited capacity is concentrated in four markets: South Africa, Nigeria, Egypt, and Kenya. Large portions of Central and Francophone Africa remain structurally underserved.

Meanwhile, demand for cloud and compute services in several African markets is expanding at rates of 35 to 40 percent annually. Industry projections suggest the continent will require between 700 and 1,000 additional megawatts of IT load within the next three to five years merely to keep pace with traffic growth and enterprise migration.

Facilities are being built. Pipelines are expanding. But in relative terms, the gap widens.

Africa’s data consumption is surging – yet the infrastructure required to process and monetize that data remains insufficient.

The result is quiet externalization. African enterprises generate data locally but often store and analyze it abroad. African consumers stream content whose caching infrastructure sits offshore. African governments digitize services that run on foreign compute clusters.

The continent is connected enough to create value — but not yet equipped to capture it.

Hyperscalers don’t create demand. They follow it

A persistent assumption in public discourse is that hyperscalers will unlock demand simply by entering African markets.

The reality is more disciplined.

Hyperscalers follow demand. They do not create it.

Their investment decisions are governed by measurable fundamentals: enterprise density, traffic concentration, power reliability, interconnection depth, and regulatory clarity. Where those variables are aligned, capital flows. Where they are fragmented, expansion pauses — regardless of demographic promise.

Demand in African markets is created by enterprises modernizing operations, telecom operators scaling broadband, fintech platforms deepening financial inclusion, governments digitizing services, and consumers embedding digital tools into daily life.

Hyperscalers respond to viable economics.

Expecting hyperscale infrastructure to precede structural readiness is to reverse cause and effect. It produces ambition without execution.

Sequencing matters. Infrastructure follows coherence.

The underrated Continent

Africa is frequently described as high-potential yet underpenetrated. A more precise description may be that it is structurally underrated because it is structurally under-visible online.

A significant number of enterprises, banks, and government networks do not operate – or do not actively use – Autonomous System Numbers (ASNs), the routing identities that provide networks with autonomy and visibility on the global internet. Traffic is often aggregated behind upstream providers, obscuring the true scale of enterprise activity.

Low IPv6 adoption further limits addressability, compressing Africa’s footprint in global internet measurement systems. From the vantage point of global platforms evaluating traffic density and growth trajectories, Africa can appear thinner than reality.

In a digital economy, visibility is infrastructure.

When demand signals are muted, investment models skew conservative. Edge nodes are delayed. Cloud regions are postponed. Capital hesitates.

Compounding this invisibility is the geography of hosting. A substantial share of African government, enterprise, and cloud workloads remains located outside the continent – in Europe, the Middle East, and the United States. Every offshore workload weakens local compute density and erodes the economic argument for hyperscale investment at home.

Africa does not lack data.

It lacks the infrastructure density – and the network visibility – to keep it.

The Big Hurdles: Power, Alignment, and Bankability

If demand is visible and capital exists, why does capacity still lag?

The answer lies in execution risk.

Power remains the most binding constraint. Data centers require stable, scalable, competitively priced electricity. Across many African markets, grid instability and regulatory rigidity force developers into expensive hybrid and self-generation models. Diesel hums behind digital ambition. Capital expenditure rises. Risk premiums widen.

But the constraint is not purely electrical.

Connectivity, energy, land, permitting, and regulatory policy are too often planned in isolation. Projects falter when anchor demand is assumed rather than contracted, when approvals move sequentially instead of in parallel, when ambition outpaces coordination.

From an investor’s perspective, these uncertainties directly affect bankability. Capital is not absent. It is disciplined. Markets that reduce ambiguity attract sustained investment. Markets that amplify uncertainty repel it.

The paradox is not a shortage of interest. It is a shortage of alignment.

What Closing the Gap Will Require

Resolving Africa’s data center paradox demands more than announcing megawatts. It requires redesigning markets.

Governments must shift from rhetoric to structured demand – acting as anchor customers for cloud services, consolidating public-sector workloads, reforming energy market rules, and harmonizing regulatory processes across agencies.

Operators must prioritize scale and interconnection. Fragmented facilities struggle to compete in a compute economy defined by density and ecosystem depth. Regional platforms and open-access models offer more durable trajectories.

Investors must back scalable infrastructure platforms capable of replication across markets – assets designed not merely to operate, but to anchor ecosystems.

Africa’s digital demand is real. It is measurable. It is accelerating.

Connectivity has reached a threshold where traffic growth is inevitable. The next chapter will not be written in fiber kilometers or cable landings. It will be written in megawatts — and in whether those megawatts sit on African soil.

The cables are already in the ground. The traffic is already flowing.

The question is whether Africa will build the infrastructure to keep what it creates — or remain a continent that generates digital value only to watch it processed elsewhere.

In the new world, terabits do not matter. What will be tracked is who owns the compute.