Hyperscale operators control half of global data center capacity, and their share is projected to rise to nearly two-thirds by 2031, according to new analysis from Synergy Research Group, highlighting a structural transformation in how digital infrastructure is deployed worldwide.

The finding that hyperscale operators control half of global data center capacity , reflects a decisive shift away from enterprise-owned infrastructure toward centralized cloud platforms designed to support artificial intelligence workloads , consumer applications, and distributed digital services.

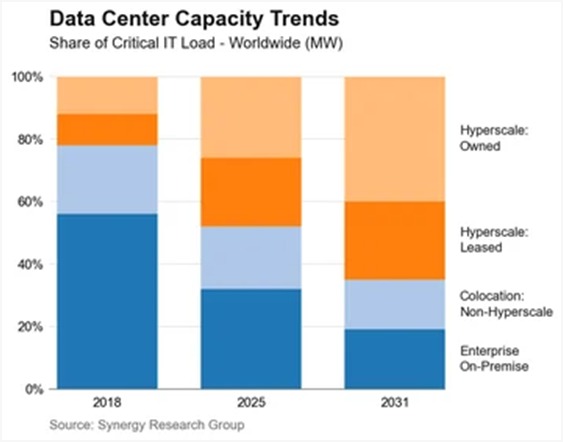

Synergy estimates that hyperscale providers currently account for approximately 48 percent of global data center capacity, with roughly 60 percent of that infrastructure located inside facilities they build and operate themselves rather than lease from third-party colocation operators.

By contrast, enterprise-owned on-premises facilities now represent about 32 percent of global capacity, while non-hyperscale colocation operators account for roughly 20 percent. These figures mark a dramatic reversal from 2018, when enterprise infrastructure dominated the global data center landscape and hyperscale expansion remained at an earlier stage of development.

The conclusion that hyperscale operators control half of global data center capacity with major providers like Amazon Web Services and Microsoft Azure leading global expansion underscores how cloud platforms have become the primary delivery architecture for digital services worldwide. It also signals how artificial intelligence workloads are accelerating investment in centralized compute environments capable of supporting high-density processing infrastructure.

Synergy projects hyperscale infrastructure capacity will expand roughly threefold by 2031. Under those projections, hyperscale providers could control as much as 67 percent of global data center capacity within five years, reinforcing the expectation that cloud platforms will remain the dominant compute layer supporting digital economies.

Chief analyst John Dinsdale said artificial intelligence has significantly accelerated infrastructure centralization trends already underway across global markets.

“Cloud and consumer-oriented digital services have been driving changes in data center deployment patterns for many years,” Dinsdale said. “But over the last three years AI technology has accelerated those changes.”

The projection that hyperscale operators control half of global data center capacity today also reflects the scale of infrastructure currently under construction worldwide. Synergy estimates that nearly 800 hyperscale facilities are already in the development pipeline, positioning the sector for another major expansion phase within the next three years.

While enterprise-owned infrastructure is expected to decline as a share of global capacity, demand for localized GPU infrastructure supporting generative AI workloads will continue to sustain growth in distributed enterprise compute environments alongside hyperscale expansion.

For African markets, the finding that hyperscale operators control half of global data center capacity highlights the growing strategic importance of attracting cloud-region investment. Countries seeking to localize compute capacity increasingly recognize that participation in the next phase of digital infrastructure development depends on securing hyperscale presence within national connectivity ecosystems.

As cloud adoption accelerates and artificial intelligence workloads reshape infrastructure planning priorities worldwide, the rise of hyperscale operators is redefining how digital capacity is financed, deployed, and integrated into national economic development strategies across emerging markets.

Related: Hyperscale capacity, cloud and African data centres