Successful deployment of localised solutions in Africa requires greater education and training, writes Wojtek Piorko, Managing Director for Vertiv (Africa).

Unprecedented customer demand for cloud services, high-quality streaming, social media and other digital services has set off a record-setting construction boom for all the major hyperscalers.

Unprecedented customer demand for cloud services, high-quality streaming, social media and other digital services has set off a record-setting construction boom for all the major hyperscalers.

Structure Research estimates that the total global hyperscale self-build capacity reached 13,117 megawatts (MW) in 2022 and an additional 13,652 MW is expected to be added over the next five to 10 years. During this time, the traditional makeup of the average data centre is changing.

Many new builds focus on efficiency, act as the hub of hybrid networks and increasingly lean on prefabricated modular solutions and design.

“Prefabricated modular data centre solutions come in the form of smaller prefabricated components, such as integrated racks, rows, aisles or skids built in the factory and deployed with servers and infrastructure included,” explains Wojtek Piorko, Managing Director, Africa at Vertiv, a global provider of critical digital infrastructure and continuity solutions. “They can also be deployed as all-in-one modules featuring integrated IT, power and thermal management. These fully integrated prefabricated modules resemble compact building blocks and can be used for new data centre builds or added to existing facilities.”

Prefabricated modular data centre solutions are built and integrated under tightly controlled factory conditions by trained specialists, which helps shorten construction timelines when time and labour are at a premium.

These solutions also help to reduce certain project costs and improve the total cost of ownership (TCO) by shortening the time it takes to start generating revenue, he says. “Depending on the architecture of the data centre, prefabricated modular designs can greatly reduce the physical footprint of the systems compared to a traditional build.”

Standardisation versus localisation: a subtle, yet important difference

Major hyperscalers often use standardised prefabricated data centre designs that allow organisations to design and engineer on the front end and repeat the build wherever they are in the world. This method may be more accepted in areas such as the United States or certain parts of the EMEA region, where there’s greater cohesion across various industry practices and regulations, adds Piorko. However, there are opportunities everywhere, and global organisations need to consider the requirements of each region before deploying a standardised solution.

Major hyperscalers often use standardised prefabricated data centre designs that allow organisations to design and engineer on the front end and repeat the build wherever they are in the world. This method may be more accepted in areas such as the United States or certain parts of the EMEA region, where there’s greater cohesion across various industry practices and regulations, adds Piorko. However, there are opportunities everywhere, and global organisations need to consider the requirements of each region before deploying a standardised solution.

“The alternative to this approach is what’s called ‘localisation’, a crucial distinction where a standardised design is slightly modified and customised to comply with local requirements. Once a solution has been localised for a specific region, it can help mitigate some of the difficulties found in traditional installations by simplifying compliance with building codes, standards and regulations.”

As far as the adoption of prefabricated modular data centre solutions goes, most of the major players in the region prefer one of three options: a fully customised solution; a solution using standard components that are combined for specific customer specifications; or a pre-designed standard solution. Each of these options provides different levels of design customisation, growth phasing/expansion capabilities, and deployment time to meet specific business requirements.

Examining the global reach of prefabricated modular data centers

EMEA

In the EMEA region, the major hyperscalers (Amazon Web Services, Google, Meta, and Microsoft) are the biggest market drivers in terms of adopting prefabricated modular data centre solutions. Hyperscalers are building in remote areas, and these wide-open spaces make it easier to deploy some of the larger, standardised modules.

In Europe particularly, there has been growing public concern regarding data centre resource consumption. To help alleviate some of these issues, hyperscalers in parts of this region have used customised elements of prefabricated modules to reclaim heat in the data centre and provide district heating for local populations.

While sustainability will continue to be a pressing topic in the region and beyond, the nature of shipping these large blocks by sea makes true sustainability a balancing act. The more that equipment providers can incorporate sustainable materials and manufacturing methods into prefab solutions, the easier it will be to balance these elements.

Africa

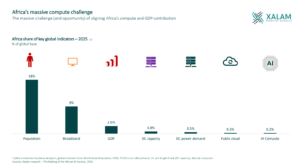

Africa has experienced massive data centre capacity growth in recent years, with expectations that the region will expand to 675 MW by 2026, according to Xalam Analytics. “While still considered an emerging market, prefabricated modular data centres have been around in Africa since 2008,” states Piorko. “Adoption in the region will continue to grow as African countries continue to pass various data privacy laws to protect personal data and allow more countries to manage their data within the continent.”

Africa has experienced massive data centre capacity growth in recent years, with expectations that the region will expand to 675 MW by 2026, according to Xalam Analytics. “While still considered an emerging market, prefabricated modular data centres have been around in Africa since 2008,” states Piorko. “Adoption in the region will continue to grow as African countries continue to pass various data privacy laws to protect personal data and allow more countries to manage their data within the continent.”

The transition from 2G to 5G, and the increased demand for data in African universities, are also driving growth for hyperscalers and colo providers in the region, he says.

“Prefabricated modular data centre solutions have been a huge help in increasing the speed to market for hyperscalers and colo providers. As we see the market grow, organisations entering the region will need to familiarise themselves with the nuances of each country to ensure they’re bringing in the right solutions, localising that solution for each region, and adding capacity without disrupting existing infrastructure.

“These considerations include climate differences, local construction codes, certifications, standing contracts, and import duties between individual components versus a full solution. Similar to other emerging regions, the challenge of finding skilled labour looms large across the African continent,” he comments. “The rapid deployment of standardised prefabricated solutions has made them more popular for hyperscalers and colo providers in Africa. However, proper education is still needed to ensure successful deployments.”

According to Piorko, organisations like Vertiv are working to establish more training centres in Africa to help educate the local businesses on all types of data centre solutions. Vertiv has five training facilities in Africa with certification programmes for technicians and salespeople. Once a prefabricated module is assembled and tested in the factory, Vertiv may also send engineers from the factory team to the building site so they can provide a factory-like presence while helping local engineers install complete solutions.

North America

Prefabricated modular data centre solutions appeal to the major hyperscalers and colocation providers in North America because their speed and ease of deployment helps stabilise construction schedules at a time when organisations are trying to meet unprecedented capacity demand. According to CBRE’s 2022 North American Data Center Trends Report, organisations from the seven primary U.S. data centre market added a record 686.8 MW of net absorption of data centre space. In this region, hyperscalers and colo providers have the advantage of proximity, and the major third-party integrators have a local presence with easy access to equipment providers. This benefit allows these integrators to deliver these solutions to various parts of the region within days.

LATAM

Latin America (LATAM) is establishing itself as an emerging market for prefabricated modular data centre solutions. This is largely credited to major developments such as Google purchasing 30 hectares of land for a data centre in Uruguay in 2021 and Scala Data Centers launching the largest vertical data centre in the region last year. In this region, the costs and risks associated with new stick build data centre and changing regional markets have made the scalability of prefabricated modular solutions more appealing. While organisations moving into the LATAM region want to standardise as much as possible, they must understand the various codes and jurisdictions and correctly localise these solutions for successful deployment.

Asia-Pacific

Colocation is the most important data centre sector in the Asia-Pacific region, largely because hyperscalers often lack access to in-country staff to build data centres there. Instead, they leverage established colocation data centres with a local presence, expertise and cable connectivity to meet demand.

Even so, the region still faces the challenge of having enough data centre builders in each country to keep up with demand. While this lack of skilled labour on site would make a strong case for organisations to look into adopting more standardised solutions, there are several reasons why prefabricated modular data centres in the Asia-Pacific region are still in relative infancy compared to the rest of the world. For example, much of the local expertise lies in traditional brick-and-mortar data centre builds, and many data centre builders in the region prefer the look and feel of a traditional data centre, rather than the container-like appearance of a prefabricated modular data centre.

Additionally, supply chain woes persist in the region. The current lead times to ship these prefabricated solutions can minimise the speed to deployment benefits that prefabricated solutions typically provide.

Preparing for a prefabricated future

An Omdia global survey of 228 companies that operate their own data centre found that 52 percent already use prefabricated modular data centre technology, and a whopping 99 percent said this technology would be a part of their future data centre strategy.

“While these regions differ in how these solutions are adopted, the evidence is clear: for hyperscalers, traditional data centres are fading into the background as prefabricated, modular buildings and components become the norm,” Piorko concludes.

Interested in more information on this topic? To download the Vertiv white paper ‘2023 Hyperscale Data Center Design: A Global View of Standardization and Localization’, please click here.

To support its customers in accelerating their digitalisation efforts, Vertiv has recently launched the Vertiv™ XR App and virtual reality tools that enable in-depth exploration of its products, including prefabricated modular solutions. The app guides users through product selection and placement, using augmented reality to deliver an immersive, realistic depiction of the product in the location of their choosing, with the intent of improving understanding of how the infrastructure will support their compute and impact on the physical footprint. Download the app to find out more.