Across much of Africa, the constraint on data center and cloud expansion is no longer connectivity. It is demand.

The continent’s digital infrastructure base is larger than it has ever been. Africa today hosts roughly 60 subsea cables, 145 cable landing points, about 1.4 million kilometers of terrestrial fiber, around 150 CDN and cloud points of presence, and between 500 and 600 megawatts of live data center IT capacity. Yet the region still represents less than 1% of global compute capacity, despite accounting for about 18% of the world’s population.

This gap reflects less a shortage of infrastructure than the absence of sustained domestic workload concentration at scale. Investors build compute where they can see predictable, long-term usage. In many African markets, enterprise cloud adoption is still developing and hyperscaler regions remain limited outside a small number of hubs. As Guy Zibi, Managing Partner at Xalam Analytics, noted during a recent Africa Hyperscalers conversation, public-sector digitization often provides the earliest stable foundation for compute markets under these conditions.

Where governments localize workloads, infrastructure follows.

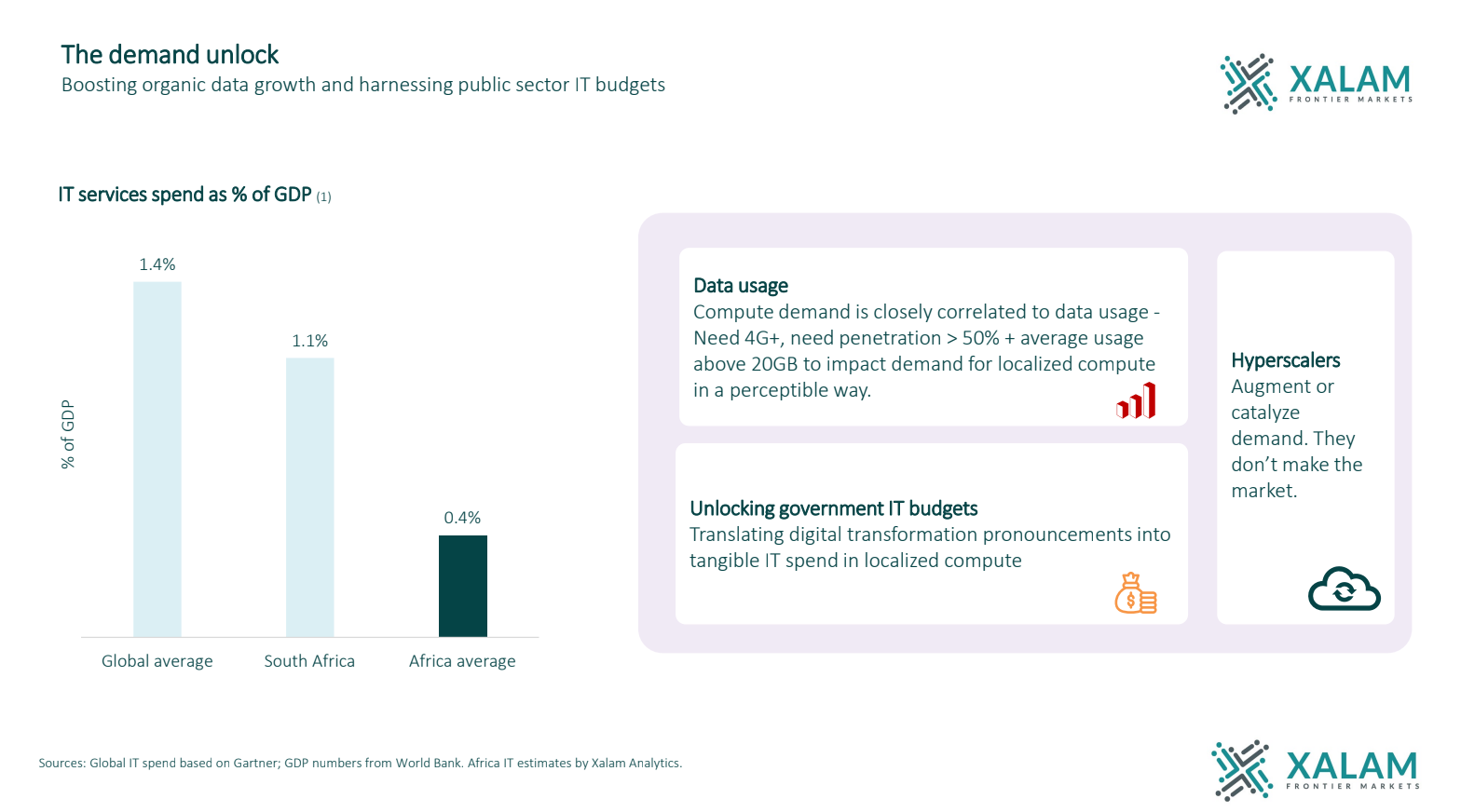

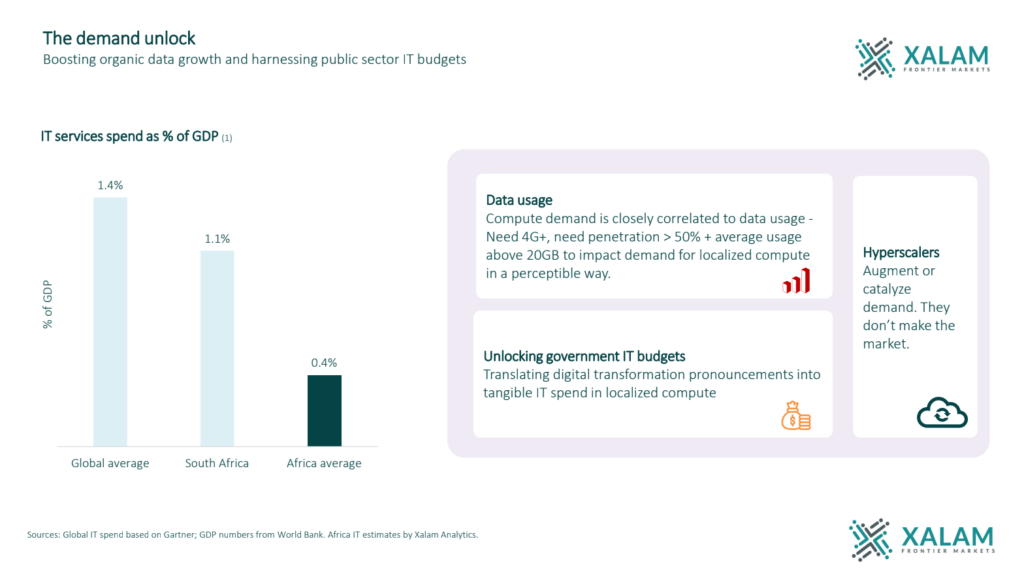

Africa’s share of global compute capacity remains small even as infrastructure expands in absolute terms. The continent accounts for roughly 0.8% of global data center capacity, about 0.3% of global public cloud usage, and approximately 0.2% of global AI compute resources. At the same time, meaningful connectivity has grown rapidly, with roughly 700 million Africans now using 4G, 5G or fiber-based broadband, a figure expected to exceed one billion by the end of the decade.

The remaining challenge is not connectivity expansion itself, but converting connectivity into persistent domestic workloads that justify local compute investment.

Public-sector platforms are among the continent’s largest generators of structured data. National identity systems, tax platforms, payment rails, land registries and health information systems all depend on secure storage, authentication layers and analytics infrastructure that must operate continuously over long time horizons. When these systems are hosted locally, they create the foundation on which broader compute ecosystems can grow.

Digital identity systems illustrate the scale of this effect. Nigeria’s national identity program has issued more than 120 million National Identity Numbers, making it one of the largest digital public infrastructure systems on the continent. Systems of this scale require persistent compute capacity and long-term infrastructure commitments that investors can rely on when evaluating market viability.

Africa’s fintech platforms and digital unicorns illustrate the same dynamic from the private sector side. Companies such as Flutterwave, OPay, Moniepoint and M-Pesa process millions of transactions daily across payments, lending and digital commerce, generating continuous streams of identity, behavioral and financial data that must be stored, secured and analyzed in real time. Systems operating at this scale depend on resilient infrastructure environments, reinforcing demand for local hosting, interconnection and cloud services and signaling growing market maturity.

Data protection and localization policies are also beginning to shape infrastructure geography across multiple African markets. Requirements that certain categories of public-sector and regulated data be hosted domestically are not only sovereignty measures. They are investment signals. They reduce uncertainty about future workload location and improve the bankability of infrastructure projects by demonstrating that demand will remain local over time.

Government action matters both as a direct source of demand and as a policy signal to the market. When governments move workloads locally and provide clarity around digital policy frameworks, they help reduce uncertainty for infrastructure investors and make markets more bankable. Regulatory clarity, procurement frameworks and national digital strategies all influence whether infrastructure ecosystems develop at scale. In early-stage compute markets, policy certainty can matter as much as consumption itself.

Government demand also plays a role in shaping energy investment tied to digital infrastructure. Data centers currently account for less than 0.5% of total electricity consumption across African markets, yet power availability remains a primary constraint on expansion because compute infrastructure depends on reliable, high-quality supply rather than simply additional capacity. Power planning across much of the continent remains largely state-led, meaning decisions about grid expansion, embedded generation frameworks and industrial tariff structures will directly influence where the next generation of African compute hubs emerges. As AI workloads increase power density requirements globally, the relationship between anchored compute demand and coordinated energy planning is becoming more important.

The absence of hyperscaler cloud regions across most African markets is sometimes interpreted as hesitation from global providers. In practice, hyperscalers rarely lead early-stage compute markets. They follow them. Public-sector workload localization helps create the demand density that signals when markets are ready for larger-scale deployment.

Africa’s digital infrastructure footprint is expanding. Connectivity has improved dramatically, and new facilities continue to come online in key markets. But the transition from connectivity growth to compute scale depends on something more durable than announcements or capacity pipelines. It depends on anchor demand.

Africa’s next generation of compute markets will not be determined only by where data centers are financed, but by where governments choose to run the digital infrastructure of their own economies.